U.S. debt, interest rates, and the opportunity in high-quality bonds

Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

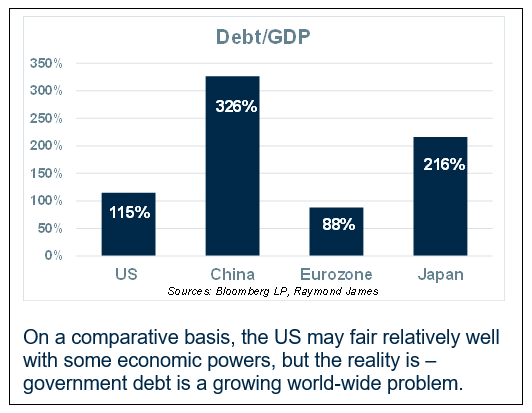

The rising debt burden of the U.S. government is becoming an increasingly serious economic concern. While it may not be an immediate crisis, it has the characteristics of a slow-moving domestic pandemic: easy to ignore in the early stages, difficult to reverse once entrenched, and capable of spreading financial pressure across households, businesses, and public institutions.

A central concern is not simply the size of the debt, but the cost of servicing it. As interest rates have risen, a growing share of federal revenue is being diverted toward interest payments rather than productive investment. When roughly one out of every five dollars of federal revenue is used to pay interest on existing debt, it limits fiscal flexibility. That means fewer resources are available for infrastructure, defense, healthcare, education, innovation, and other national priorities.

Higher debt-service costs also matter because government borrowing competes with the private sector for capital. When rates remain elevated, the impact spreads across the economy. Families face higher mortgage costs and reduced housing affordability. Homebuilders confront tighter margins and weaker demand. Childcare providers, small businesses, and other operators dependent on short-term credit face more expensive financing. Capital-intensive sectors such as energy infrastructure, artificial intelligence development, hospital systems, manufacturing, and research and development all become harder to fund. While this is not an exhaustive list, it serves to illustrate the impact. Over time, this can suppress investment, productivity, and long-term growth.

The reverse is also true. A credible path toward reducing the debt burden would likely ease pressure on borrowing costs, improve confidence among consumers and businesses, reduce inflation concerns, and strengthen the foundation for sustainable economic growth. Lower government financing needs could create more room for private investment, making capital more available to families and businesses.

There are several forces putting upward pressure on rates. One is the strength of the U.S. economy. Corporate earnings have been surprisingly resilient, business activity has remained solid, and investment tied to artificial intelligence has contributed to growth expectations. Strong growth can support higher rates because investors demand compensation for the possibility that inflation and demand will remain firm.

Inflation is another major factor. Even when inflation stops accelerating, prices that remain elevated continue to erode purchasing power. This is an important point that is often missed. Consumers and investors can become desensitized to inflation over time, but stagnant inflation is not harmless. If prices remain high and wage gains fail to fully offset the increase in living costs, household standards of living gradually deteriorate. The damage is cumulative. The purchasing power of the dollar continues to weaken, even if the pace of price increases appears less alarming than before.

A third factor is perceived creditworthiness. If investors begin to question the long-term fiscal discipline of the United States government, they may demand higher yields to hold Treasury debt. The US still benefits from deep capital markets, the dollar’s reserve currency status, and the perceived safety of Treasury securities. Those advantages are powerful, but they should not be taken for granted. Persistent deficits, political dysfunction, and rising debt-service costs can gradually weaken investor confidence.

That said, the debt discussion requires balance. Not all borrowing is inherently harmful. Debt used to fund productive investments can enhance future growth if it raises productivity, improves infrastructure, strengthens national competitiveness, and/or supports innovation. The issue is whether debt growth is paired with a credible return on investment and a sustainable fiscal framework. Borrowing that merely funds ongoing consumption without improving future capacity is far more problematic.

There is also no painless solution. Reducing debt growth may require some combination of spending restraint, entitlement reform, tax changes, faster economic growth, and greater fiscal discipline. Each option carries political and economic tradeoffs. Moving too aggressively toward austerity could weaken growth, while doing too little could allow interest costs to consume an even larger share of federal resources. The challenge is finding a credible path that stabilizes debt without undermining the economy’s productive base.

For investors, the current fixed income environment presents both risks and opportunities. Higher yields over the last three years have created the opportunity for stronger fixed income returns than investors had experienced during the previous 15+ years. Today’s bond market allows investors to earn meaningful income while reducing unnecessary risk. This is particularly important for investors who do not need to reach for lower-quality credits to generate acceptable yields.

In this market, high-quality bonds deserve renewed attention. Laddered portfolios can help manage reinvestment risk, reduce the need to make precise interest-rate forecasts, and provide a disciplined structure for income generation. Because no investor can know the future path of rates with certainty, a laddered approach can help balance flexibility, income, and risk control.

There is no perfect strategy for an uncertain market. But investors do not need perfection to make sound decisions. They need to recognize what the market is currently offering, understand the risks embedded in the broader economic backdrop, and align opportunities with their individual objectives. Today, that means acknowledging the seriousness of the U.S. debt trajectory while also recognizing that higher-quality fixed income now offers more compelling return potential than it has in many years.

The debt problem will not be solved quickly. It will require discipline from policymakers and realism from investors. But the market is already providing signals. Elevated rates reflect inflation concerns, fiscal pressure, resilient growth, and questions about the long-term cost of capital. Investors who respect those signals and build portfolios around quality, income and structure, may avoid unnecessary speculation and be better positioned for the period ahead.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.